The Single Strategy To Use For Business Insurance Agent In Jefferson Ga

Table of ContentsAuto Insurance Agent In Jefferson Ga Can Be Fun For EveryoneSee This Report on Insurance Agent In Jefferson GaExamine This Report about Business Insurance Agent In Jefferson GaThe Home Insurance Agent In Jefferson Ga Statements

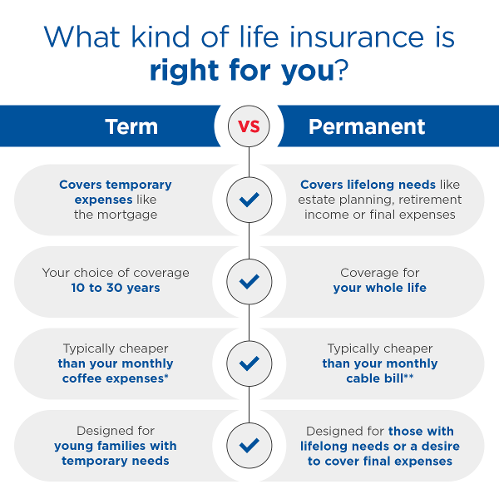

Learn a lot more concerning just how the State of Minnesota supports active duty members, experts, and their families.Term insurance coverage provides security for a specified time period. This period could be as short as one year or provide coverage for a particular number of years such as 5, 10, 20 years or to a defined age such as 80 or in many cases as much as the oldest age in the life insurance death tables.

The longer the warranty, the greater the initial costs. If you die during the term duration, the business will pay the face quantity of the policy to your recipient. If you live beyond the term duration you had selected, no benefit is payable. As a rule, term plans offer a fatality benefit without cost savings element or cash money value.

Some Known Incorrect Statements About Home Insurance Agent In Jefferson Ga

The costs you pay for term insurance are lower at the earlier ages as compared to the costs you pay for long-term insurance coverage, but term prices rise as you age. Term plans might be "convertible" to an irreversible strategy of insurance policy. The insurance coverage can be "level" supplying the same advantage till the plan expires or you can have "lowering" insurance coverage during the term duration with the premiums remaining the same.

Currently term insurance rates are very competitive and among the most affordable traditionally experienced. It should be noted that it is an extensively held belief that term insurance coverage is the least costly pure life insurance policy coverage offered. https://www.wattpad.com/user/jonfromalfa1. One requires to examine the plan terms very carefully to determine which term life alternatives are ideal to meet your particular situations

The size of the conversion duration will certainly differ depending on the type of term policy bought. The costs rate you pay on conversion is generally based on your "current acquired age", which is your age on the conversion date.

Under a level term plan the face amount of the plan stays the same for the whole period. Frequently such plans are offered as home mortgage security with the amount of insurance coverage decreasing as the equilibrium of the mortgage lowers.

The Single Strategy To Use For Home Insurance Agent In Jefferson Ga

Commonly, insurance providers have not deserved to alter premiums after the policy is marketed. Considering that such policies might continue for years, insurance firms need to utilize conservative death, rate of interest and cost rate quotes in the premium computation. Adjustable premium insurance policy, nevertheless, permits insurance providers to use insurance coverage at reduced "current" costs based upon less conventional assumptions with the right to change these premiums in the future.

Sometimes, there is no relationship between the size of the cash worth and the premiums paid. It is the cash worth of the plan that can be accessed while the insurance holder lives. The Commissioners 1980 Criterion Ordinary Death Table (CSO) is the current table utilized in determining minimum nonforfeiture values and plan reserves for regular life insurance policy plans.

The policy's essential aspects contain the premium payable annually, the death benefits payable to the beneficiary and the money abandonment value the policyholder would obtain if the policy is surrendered prior to fatality. You might make a car loan against the cash money value of the policy at a specified interest rate or a variable price of rate of interest however such impressive loans, otherwise paid off, will reduce the death benefit.

All About Auto Insurance Agent In Jefferson Ga

If these estimates transform in later years, the business will change the costs appropriately yet never ever above the optimum guaranteed premium mentioned in the policy. An economatic whole life plan attends to a standard amount of taking part whole life insurance policy with an extra supplementary insurance coverage offered via the use of rewards.

Ultimately, the reward additions need to equal the original amount of supplemental coverage. Since dividends may not be adequate to acquire enough paid up additions at a future date, it is feasible that at some future time there can be a considerable decline in the quantity of additional insurance policy coverage - https://public.sitejot.com/jonfromalfa1.html.

Due to the fact that the costs are paid over a much shorter period of time, the costs repayments will be higher than under the whole life plan. Solitary premium whole life is limited payment life where one huge superior payment is made. The plan is totally paid up and no additional costs are required.